Lazy guide to saving smart in Canada

I HATE saving.

As a lazy person I hate having to do things more than once. Having to think about my finances, savings strategy, and retirement goals at 23 year old is generally not fun and if you're anything like me you probably feel hopelessly lost when figuring out what to do with your extra loonies and toonies. To solve this I built a dead easy strategy so I don’t need to keep worrying about it.

Disclaimer: While this strategy works for me and I don’t see any reason it couldn’t work for the vast majority of people it’s definitely not for everyone and can always be improved. If you have suggestions feel free to tell me @ImNickDev!

Disclaimer: While this strategy works for me and I don’t see any reason it couldn’t work for the vast majority of people it’s definitely not for everyone and can always be improved. If you have suggestions feel free to tell me @ImNickDev!

Step 0: Be Cash Flow Positive

As a person who put themselves through university while living on my own I will be the first to say this is definitely easier said than done but you gotta be making money before you can save it. The only advice I have is often times your spending is much easier to control than your income, so to get into a positive cashflow take a hard look at your spending habits, break out the scissors, and start cutting. I have been lucky to have some amazing influences in my life. My mom as a single parent was able to raise 6 children on less than $30k/year and all I can say is where there is a will there is generally a way.

Step 1: Get the right vehicle for the job 🏎

You wouldn’t use a ferrari to move your couch, so why use a checkings account to save for retirement. This is a obvious for some but not all; my optimal lazy saving strategy requires 3 accounts:

You wouldn’t use a ferrari to move your couch, so why use a checkings account to save for retirement. This is a obvious for some but not all; my optimal lazy saving strategy requires 3 accounts:

- 💵Parking Account: Something with a high interest rate that is hard to get money out. I suggest EQBank as it provides a 2.3% interest rate (double what most chequing accounts offer) and there is no debit card meaning it’s easier to save and harder to spend out of impulse. Edit: Worth noting EQBank offers unlimited EFTs and free e-transfers so you can access your money quickly if needed.

- 💸Spending Account: Something with NO fees and cash back credit card. I suggest Tangerine as fit both these criteria and offer a pretty great user experience all around. Edit: Use my code ‘45973813S1’ and we both get $50 free for your first deposit, it’s appreciated if you do👍

- 💰Saving Account: Hold registered accounts (TFSA and RRSP) and have minimal MER’s and fees. I suggest Wealthsimples robo-advisor because its dead easy to use, has none of the hidden fees or inflated MER’s most big banks have, and they continue to push forward modern online banking.

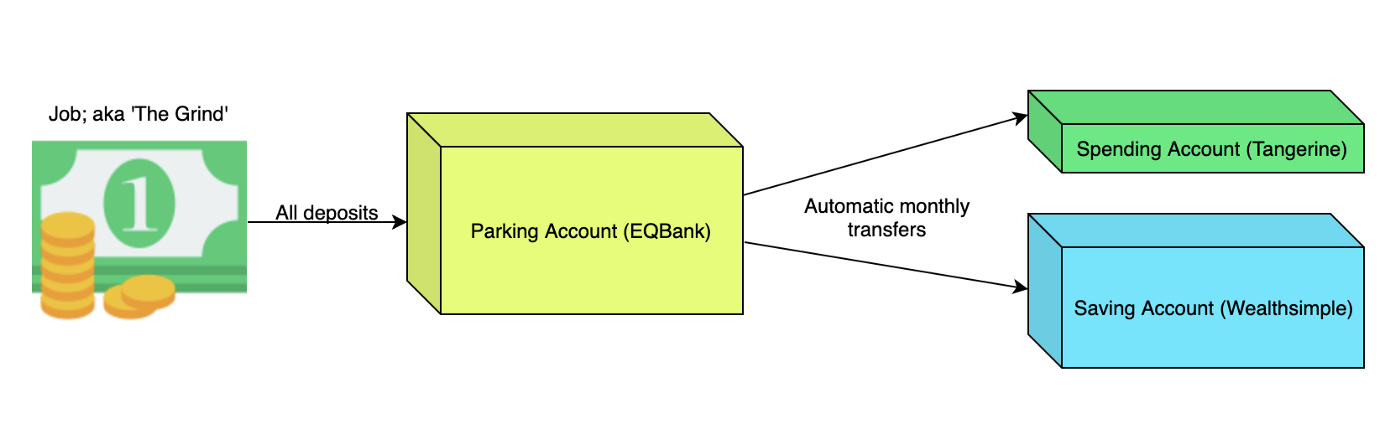

Step 2: Put them all together 📎

Now you might be thinking “Nick this was hard enough before when I have one account, how is this is going to be easier with 3 accounts?!”, it’s a valid concern but trust me optimal laziness is coming! Just follow this diagram:

Now you might be thinking “Nick this was hard enough before when I have one account, how is this is going to be easier with 3 accounts?!”, it’s a valid concern but trust me optimal laziness is coming! Just follow this diagram:

Once you get get your direct deposits going to your parking account all you need to do is setup 2 automatic recurring transactions; the first one to your spending account with all your monthly expenses (rent, utilities, misc, etc) and the second with whatever amount your comfortable sending to your savings account.

Step 3 (optional): Rules of thumb 👍

By this point your pretty rock solid. You no longer are paying any dumb fees to banks, you are setting up barriers to protect you from impulse spending, and your have the almighty power of compound interest on your side! In only a day or two you have netted thousands to tens of thousands down the road so you should give yourself a hand 👏👏👏. Now if you feel like you want to put a little more time in here are some rules I like to follow:

- Emergency Fund: Never have more than 6 months total for expenses in cash (Parking Account). If you have contribution room in your TFSA or RRSP seriously consider making a contribution. Exceptions include immediate plans to buy a house or other large investment (not “I think I might buy a house maybe sometime soon ish” 😤).

- RRSP or TFSA?: If you think your income will be more next year than this year prioritize TFSA over RRSP and vise versa. Wealthsimple will tell you what your contribution limits are for these accounts.

- Monthly or annual contributions?: Once January rolls around if your financial situation supports it you should put as much of your TFSA contribution amount as you can. If you are limited to monthly contributions there is no reason to be concerned.

- Free Banking vs Student Banking?: Do your future self a favour and switch to a free banking option NOW. When you graduate you’re probably gonna forget to cancel it and worse your gonna be worried about graduation, jobs, loans, etc. Unless you have pretty specific needs most free banking options offer similar experiences to the student accounts.

- Points program or cashback?: Cash is king; period. It’s possible you have a points program that compliments your life style but for most people a normal cashback card will net you $12 in about the same time you get the scene points to buy a movie ticket.

- “My mom/dad/uncle/guy in a internet article told me to…”: If anybody tries to tell you need to do exactly what they’re doing financially it’s always good to question it and be objective when you research (especially when it’s ‘guy in a internet article’).

Caveats and Extras 🚫

- Most of this is just simplified info from the kind folks on /r/PersonalFinanceCanada and /r/fican

- There are absolutely alternatives to my banking suggestions (and maybe some better ones you can find) I purposely provided only one example cause if I did more than one you would need to do research and that’s not lazy

- This article doesn’t mention much about carrying debt which is becoming surprisingly more common for young people. If you are carrying debt and you want to do what’s best for you I encourage you to post on /r/PersonalFinanceCanada and see what the great people there might suggest for your situation.

- I’m just as qualified as your local Subway sandwich artist or TD financial advisor to give you this advice so take it with a BIG grain of salt.

If you enjoyed this article please share it with anyone you think would like it 🙇♂️, if you have comments I usually respond on twitter, and best of luck with your lazy savings! 😴